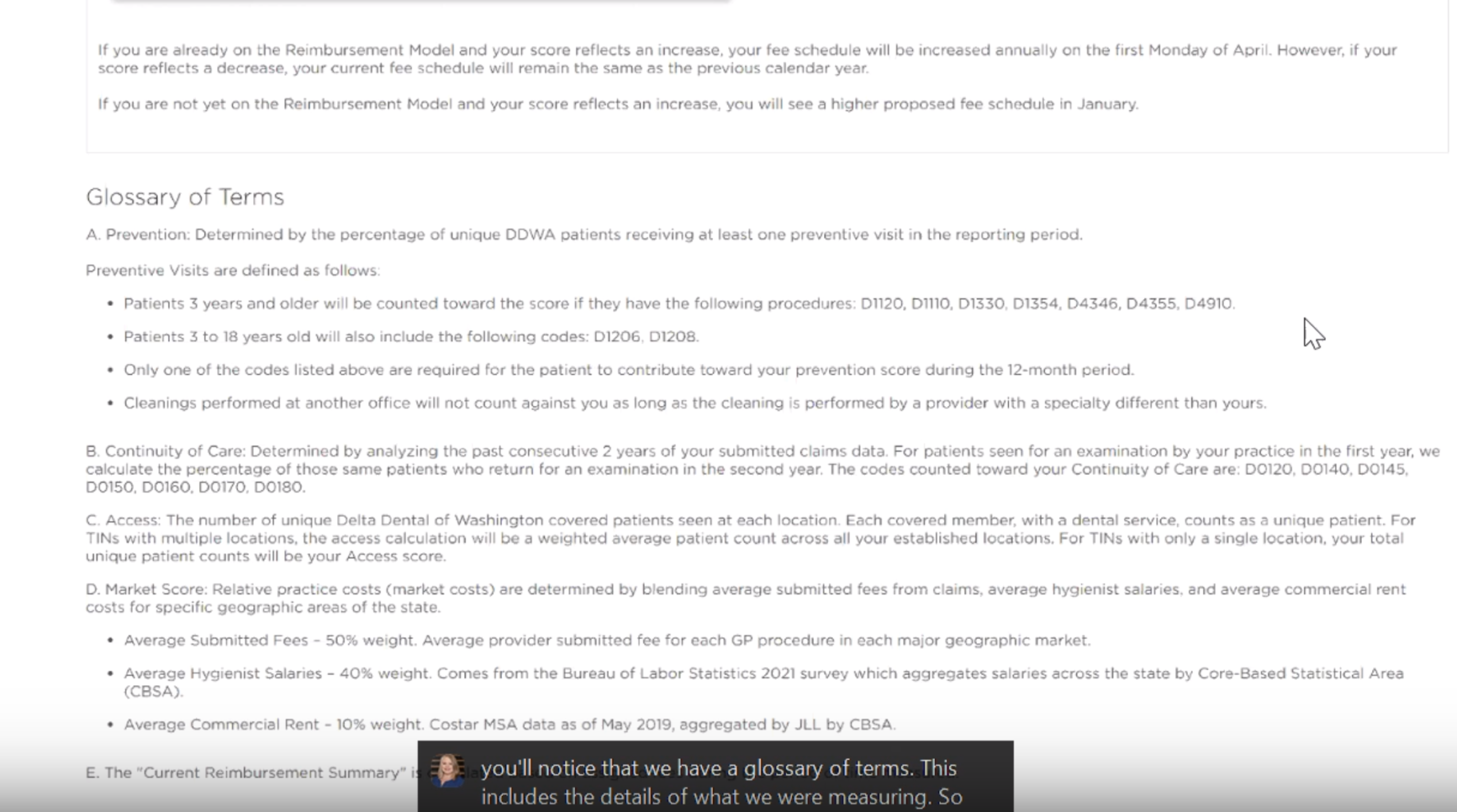

| ⚠️ SCAM ALERT: If you

The actual cost of a Washington State annual report is $70 for most for-profit businesses. Third-party mailers routinely charge $100–$200 or more for filings that may not be necessary at all. |

Scam Alert: Washington Annual Registration Mailers Are Back in 2026

If your dental practice, PLLC, or other Washington LLC recently received a letter titled “2026 Annual Registration — Final Reminder” or “2026 Annual Registration Instruction Form,” pause before you pay. A new wave of these misleading mailers has been circulating in Washington State in 2026, and they are designed to look far more official than they are.

We are flagging this for our clients because the dental industry — where practices are commonly structured as PLLCs or S-Corps — is a frequent target. These letters are not from the Washington Secretary of State. They are from private, third-party companies that charge excessive fees for services that are either unnecessary or available directly from the state at a fraction of the cost.

What the Mailer Looks Like

The notice below is an example of one currently circulating in 2026. Notice that it includes legal-sounding language, RCW statute references, urgent “respond by” dates, and even an ALERT box warning recipients about other imposter letters — while itself being a third-party solicitation from a company called “Fast Filing Services.”

Example of a third-party mailer

circulating in 2026. Client address has been redacted. This letter is not from

the Washington Secretary of State.

Note the fine print at the top right: “Beware of imposter letters that have been circulating around Washington. We are not associated with Next Step Filings.” This is a telling detail. The letter is essentially a third-party service trying to differentiate itself from other scammers — while engaging in the same practice of charging excessive fees for state filings you can do yourself for $70.

This Is Not New — Washington Businesses Have Been Targeted for Years

The Washington Attorney General’s Office has issued repeated warnings about fraudulent Secretary of State notices targeting small businesses across the state. According to the Attorney General, these scam letters are designed to mimic official government communications and demand payment well beyond the cost of legitimate state business filings.

These letters are addressed directly to businesses, often include the company’s Unified Business Identifier (UBI) number, and may include the Washington state seal — all of which make them appear official. However, business names and UBIs are publicly available records, not confidential information. Anyone can look them up and use them to make a solicitation appear legitimate.

Multiple consumer protection lawsuits have been filed and won by the Attorney General’s Office against companies engaging in this conduct, with courts imposing civil penalties and ordering restitution. The schemes keep resurfacing under new company names.

How to Tell the Difference: Scam vs. Legitimate SOS Notice

Use this table to evaluate any annual registration notice you receive:

Check This | Scam / Third | Legitimate WA |

Sender/Return Address | Private company (e.g., Fast Filing Services, Next Step Filings, | sos.wa.gov or official SOS letterhead. Mailed from Olympia, WA. |

Fees Requested | Often $100–$200+ for a filing that may not be needed at all. | Annual report fee is $70 for for-profit businesses. No other fees |

Urgency vs. Actual Due Date | Creates a “respond by” date that is weeks or months earlier than | Sends notice ~60 days before your expiration month. Your actual |

QR Codes / Website URLs | QR codes link to .org, .com, or other non-government sites. | All official links end in .gov (sos.wa.gov). The SOS does not |

Legal-Sounding Language | Quotes RCW statutes and threatens administrative dissolution to | Communicates plainly. Does not reference competitors or unrelated |

How to Verify | Google the company name. Check the WA Secretary of State CCFS | Call (360) 725-0377 or email co***@****wa.gov to confirm the |

Red Flags in the Specific 2026 Mailer

The letter shown above has several specific characteristics that identify it as a third-party solicitation rather than an official government notice:

• Two different dates: The letter shows a “Please Respond By” date of 3/27/2026 but a “Due Date” of 6/30/2026. The real filing deadline is 6/30 — the earlier date is designed to create artificial urgency and pressure you to pay quickly.

• Sent by “Fast Filing Services,” not the Secretary of State: The bottom of the letter references this private company. The Washington Secretary of State does not contract private third parties to collect annual report fees.

• Warning about other scammers: The ALERT box disclaiming association with “Next Step Filings” is itself a red flag. The real Secretary of State has no reason to disclaim being associated with other private companies.

• RCW citations used as legitimacy props: Quoting Washington state statutes sounds official, but any private company can quote state law. The citation does not mean the mailer is from a state agency.

• No official Secretary of State branding: Legitimate correspondence from the Secretary of State’s office clearly identifies the agency, uses .gov email addresses, and links to sos.wa.gov. Third-party letters often omit or obscure this.

What the Real Filing Actually Costs

The Washington Secretary of State annual report fee is $70 for most for-profit businesses (including PLLCs and S-Corps). There are no additional required fees for a standard annual report filing.

You can file directly at: sos.wa.gov → Corporations and Charities Filing System (CCFS)

The Secretary of State sends its own reminder notices — by email approximately 60 days before expiration and by mail 45–60 days before expiration if you have not selected electronic notification. These notices come from the SOS directly, not from third-party services. |

What to Do If You Received One of These Letters

1. Do not pay. Set the letter aside and verify your actual filing status first.

2. Go to sos.wa.gov and log in to the Corporations and Charities Filing System (CCFS) to check the status of your annual report. You can see whether your filing is current, when it is due, and what you owe — at no cost.

3. If you are unsure whether a notice is legitimate, contact the Secretary of State’s office directly: call (360) 725-0377 or email co***@****wa.gov.

4. If you determine the letter is fraudulent, report it to the Washington Attorney General’s Office at atg.wa.gov. The more complaints received, the better the AG’s ability to take action against these companies.

5. Forward the letter to your DAG advisor.

What to Do If You Already Paid

| If you have already sent payment to a third-party company for a Washington annual registration filing, consider taking these steps:

• Contact your bank or credit card company immediately to stop or dispute the payment. • File a complaint with the WA Attorney General at atg.wa.gov. • Check sos.wa.gov to verify the status of your actual annual report. If the third party filed it on your behalf, your information (and payment) may now be in someone else’s name. • Contact the SOS at (360) 725-0377 if you find an unauthorized filing under your business name. |

Official Resources

• Washington Secretary of State CCFS: sos.wa.gov —

verify your filing status and file your annual report directly

• SOS Phone: (360) 725-0377

• SOS Email: co***@****wa.gov

• Misleading Notices FAQ (SOS): sos.wa.gov →

search “Misleading Notices & Solicitations”

• Report a Scam (WA AG): atg.wa.gov → File a

Consumer Protection Complaint

Disclaimer: This article is prepared by Dental Accounting Group (DAG) for general informational purposes only and does not constitute legal, tax, accounting, or investment advice. Information is based on sources believed to be reliable as of the publication date. Individuals and businesses should verify their specific circumstances directly with the Washington Secretary of State. To report a scam, contact the WA Attorney General’s Office at atg.wa.gov.

© 2026 DG Accounting Professionals LLC. All Rights Reserved. |