A busy day in a dental practice might include hygiene appointments, restorative procedures, insurance coordination, and conversations about treatment plans. Behind every one of those interactions is a financial system that supports the practice, from payroll and equipment costs to patient billing and reimbursements.

Because dentistry operates on tight schedules and steady cash movement, taxes play an important role in the practice’s overall financial stability. Every procedure, insurance reimbursement, and patient payment contributes to the practice’s income and ultimately affects its tax obligations.

Many dental practice owners approach taxes as a once-a-year obligation tied to filing a tax return. In reality, tax planning plays a significant role in how cash moves through the practice throughout the tax year. When tax strategies are reviewed consistently during the calendar year, dentists gain greater control over tax liabilities, improve cash flow, and build a stronger financial structure for long-term growth.

Dental Accounting Group in Bellevue, WA works exclusively with dental professionals. Through proactive planning, custom financial reporting, and strategic advisory support, dental practices gain a clear view of their financial situation and the steps that can help them manage taxes effectively.

Why Tax Planning Matters for Dental Practice Cash Flow

Taxes influence nearly every aspect of a practice’s financial structure. A dental office generates income through patient payments and insurance reimbursements while also managing expenses related to staffing, equipment, technology, and supplies. Each of these factors contributes to taxable income and affects the final tax bill.

Without proactive planning, dentists often discover tax obligations after the year has already closed. At that point, options for adjusting deductions or implementing tax strategies are limited.

When tax planning takes place throughout the current year, dental practices gain opportunities to manage their gross income, review deductible expenses, and adjust financial decisions before filing the next return. This approach helps stabilize cash flow and supports the practice’s financial goals.

Proactive planning also helps dentists anticipate tax payments and avoid unexpected financial strain when tax deadlines arrive. For dental practices working with a dental-focused accounting partner, these reviews can happen consistently throughout the year, helping practice owners understand how financial decisions today may influence tax obligations and cash flow later.

What Is Proactive Tax Planning?

Proactive tax planning involves reviewing financial activity regularly throughout the year and identifying opportunities to improve tax efficiency. Instead of waiting for a tax preparer to compile numbers after the fact, dentists work with a tax advisor or tax professional who helps guide financial decisions in real time.

This process includes reviewing financial statements, tracking adjusted gross income, analyzing practice expenses, and planning how business income will affect the practice owner’s personal tax situation.

The goal is clear. Dentists want to reduce unnecessary tax burden while maintaining full tax compliance under current tax laws in the United States.

Proactive planning also allows the accounting team to evaluate the practice’s tax bracket, estimate potential tax liabilities, and explore legitimate opportunities for tax savings before the end of the year. A dental accounting team that reviews financial activity regularly can help practice owners identify these opportunities earlier, allowing tax strategies to be implemented before the year closes.

How Taxes Affect the Cash Flow of Dental Practices

Cash flow determines how easily a dental practice can pay team members, invest in equipment, and maintain daily operations. Taxes influence that cash flow in several ways.

First, taxes determine how much income remains available after expenses. When tax liabilities are higher than expected, the practice may need to divert funds that were originally allocated for other priorities.

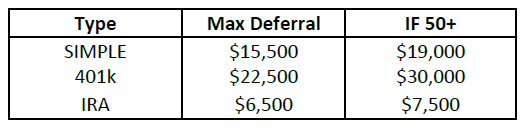

Second, taxes influence planning decisions related to investments and long-term financial goals. For example, contributions to retirement accounts, including a traditional IRA or Roth IRA, may provide both retirement planning benefits and tax advantages.

Third, taxes affect how dentists structure financial decisions throughout the year. Equipment purchases, property taxes, payroll adjustments, and other deductible expenses can influence taxable income.

With careful planning, dentists gain more control over these variables and protect the financial stability of their practice. With guidance from a dental CPA who understands the financial structure of dental practices, these variables can be reviewed throughout the year to support healthier cash flow and more predictable financial planning.

How Strategic Tax Planning Reduces Financial Surprises

Unexpected tax bills create stress for many business owners. Dental professionals often experience this challenge when tax planning occurs only after the calendar year ends.

Regular financial reviews with a tax advisor help eliminate these surprises. Instead of reacting to numbers during tax season, dentists monitor financial activity throughout the year.

This process may involve reviewing estimated income tax obligations, tracking tax withholding estimator calculations, and evaluating potential deductions related to business expenses.

A proactive approach helps dental practices maintain awareness of their tax situation and adjust financial decisions before deadlines approach. As a result, tax payments become predictable and easier to manage within the practice’s cash flow structure. Ongoing communication with a dental accounting advisor helps ensure that potential tax obligations are reviewed early, giving practice owners time to adjust financial decisions before deadlines arrive.

What Financial Areas Should Dental Practices Review During the Tax Year?

Effective tax planning involves several areas of financial review. Dental Accounting Group encourages dentists to monitor financial records and practice performance consistently throughout the year.

Important areas of focus often include:

- Tracking deductible expenses related to equipment, supplies, and operations

- Reviewing tax records and financial statements regularly

- Monitoring changes in income that may affect the practice’s tax bracket

- Evaluating opportunities for tax credits and available deductions

- Reviewing payroll structures and tax withholding requirements

- Planning retirement contributions through retirement accounts

These ongoing reviews help the accounting team identify opportunities for tax savings while maintaining compliance with current tax code requirements. Reviewing these areas with an experienced dental accounting team allows practice owners to stay organized while identifying opportunities for tax savings that align with the practice’s broader financial goals.

How Do Tax Strategies Support Long-Term Financial Goals?

Tax strategies influence both short-term cash flow and long-term financial stability. Dentists who plan ahead gain the ability to align financial decisions with their broader professional goals.

For example, retirement planning often plays a major role in tax strategy. Contributions to an individual retirement account or employer-sponsored retirement plan may reduce taxable income while helping dentists build long-term savings.

Other planning considerations may include:

- Structuring business income to improve tax efficiency

- Reviewing capital gains tax implications for investments

- Monitoring investment earnings from mutual funds or other financial assets

- Evaluating deductions related to property taxes or mortgage interest

- Planning charitable donations or charitable contributions

These decisions influence how income is taxed and how financial resources accumulate over time. A thoughtful tax strategy allows dentists to pursue financial goals while maintaining a clear understanding of how tax obligations affect those plans.

With consistent financial reporting and advisory support, dentists can evaluate these strategies with clarity and ensure that tax decisions support both short-term operations and long-term financial planning.

Why Dental Practices Benefit From Specialized Tax Expertise

Dentistry presents unique financial challenges compared with many other industries. Dental practices manage a blend of healthcare services, insurance reimbursements, and private patient payments. Equipment investments and facility costs also contribute to complex financial structures.

A tax preparer or accounting firm that works specifically with dental professionals understands these patterns. A dental CPA recognizes how financial reports, payroll, and insurance billing influence the practice’s taxable income.

Specialized dental accounting services allow the accounting team to analyze financial data within the context of the dental industry. This perspective supports more effective tax planning and stronger financial management.

For dental practice owners, working with an experienced accounting partner provides reassurance that financial decisions align with both industry realities and current tax laws.

What Role Does Communication Play in Effective Tax Planning?

Strong communication between the dental practice and the accounting team remains essential for effective planning.

Tax planning requires up-to-date information about revenue, expenses, and operational changes within the practice. When dentists communicate regularly with their accounting advisor, financial decisions can be evaluated quickly and accurately.

This collaborative approach allows the accounting team to review financial statements, track changes in income, and provide guidance before the tax year ends.

Consistent communication also supports better decision-making. Dentists gain clarity about how equipment purchases, payroll adjustments, or other financial actions may influence their tax situation.

Can Tax Planning Improve Profitability for Dental Practices?

Yes. Strategic tax planning helps dental practices retain more of their income by identifying opportunities for tax efficiency while maintaining full compliance with federal and state requirements.

When dentists work with a qualified tax professional throughout the year, they gain visibility into their financial performance and the tax implications of business decisions. This awareness supports better cash flow management, reduces unnecessary tax burden, and strengthens overall profitability.

Partner With Dental Accounting Group for Strategic Tax Planning

Dental practice owners benefit from financial guidance that extends beyond basic tax preparation. A proactive approach to tax planning supports clearer financial management, stronger cash flow, and greater confidence in long-term planning.

Dental Accounting Group provides accounting and advisory services built specifically for dental professionals. From dental-specific bookkeeping and payroll coordination to financial reporting and strategic advisory support, the firm helps dentists maintain organized financial records and make informed financial decisions.

By reviewing financial activity throughout the year, the team helps dental practices identify tax strategies, monitor tax liabilities, and prepare for upcoming tax obligations with clarity.

Connect with Dental Accounting Group to learn how specialized dental accounting services can support your practice’s goals.

Disclaimer: This article is intended for general informational purposes only and does not constitute legal, tax, or professional advice. Every situation is unique, and tax laws are subject to change. You should consult with a qualified tax professional or CPA regarding your specific circumstances before making any decisions based on this information. This content is provided in accordance with AICPA professional standards and does not create a client relationship with Dental Accounting Group.